|

If you’re trying to decide if you’re ready to buy a home, there’s probably a lot on your mind. You’re thinking about your finances, today’s mortgage rates and home prices, the limited supply of homes for sale, and more. And, you’re juggling how all of those things will impact the choice you’ll make. While housing market conditions are definitely a factor in your decision, your own life and your finances may be even more important. As an article from NerdWallet says: “Housing market trends give important context. But whether this is a good time to buy a house also depends on your financial situation, life goals and readiness to become a homeowner.” Instead of trying to time the market, it may help to focus on what you can control. Here are a few questions that can give you clarity on whether you’re ready to make your move. 1. Do You Have a Stable Job? One thing to consider is how stable you feel your employment is. Buying a home is a big purchase, and you’re going to sign a home loan stating you’re going to pay that loan back. That can feel like a big obligation. Knowing you have a reliable job and income coming in can help put your mind at ease. As NerdWallet explains: “A mortgage is a big commitment . . . Wait until your employment is stable before thinking about buying a house.” 2. Have You Figured Out What You Can Afford? To make sure you have a good idea of what you’ll need to save and what you can expect to spend on your monthly payment, talk to a trusted lender. They’ll be able to tell you about the pre-approval process and what you can borrow, current mortgage rates and approximate monthly payments, closing costs to anticipate, what percent of the purchase price of the home you’ll need for a down payment, and more. The best part is you may find out you’re closer to your goals than you realized. You don’t necessarily need to put 20% down, unless it’s specified by your lender or loan type. As Down Payment Resource says: “A 20% down payment on a home is great, but . . . Many mortgages require no more than 3% to 5% of the purchase price as a down payment. Plus, there are loans and grants that may help cover these costs. Search for down payment assistance in your area, and discuss your results with your mortgage lender . . .” 3. How Long Do You Plan to Live There? Another important thing to think about is how long you plan to stay put. It takes time to build equity in your home through paying down your loan and home price appreciation. If you plan to move too soon, you may not recoup your investment. For example, if you’re looking to sell and move again in a year, it might not make sense to buy right now. As a recent article from CNET says: “Buying a home is a good idea if you’re planning to stay put for at least three years. Home values typically increase between 2% and 5% annually, so you could end up paying more in closing costs than you’d earn in proceeds if you sell after only a year or two.” So, think about your future. If you plan to transfer to a new city with the upcoming promotion you’re working toward or you anticipate your loved ones will need you to move closer to take care of them, that’s something to factor in. Above all else, the most important question to answer is: do you have a team of real estate professionals in place? If not, finding a trusted local agent and a lender is a good first step. Bottom Line If you’re trying to decide if you’re ready to buy a home, these questions can help. But ultimately, your best and more reliable resource is the help of trusted real estate professionals. Let me know how I can help! Im just a phone call or email away! Source

0 Comments

Buyers are still looking, potential sellers are hesitating. Inventory is low and overall days on market have increased. Still a perfect time to buy and sell!

Buyers: Discuss your financing and down payment assistance options with a lender. Ask me about new build offers and incentives! They are really pushing these out as the year comes to an end! Sellers: Ask me about your Buy Before You Sell options and find out if your current mortgage can be assumed by the buyer for an even more enticing incentive! When you’re selling your home or making an offer to buy one, price is an important decision. How do you choose a number to attract the highest offers or get your offer accepted without overpaying? Consider the following: Where Is It? You know location matters, but keep in mind that even small differences can increase or decrease the desirability and price of a home. One side of a street may have a better view, the next block over can be zoned for a different school district, or a tranquil setting can be only a short distance away from noise and traffic. Be Careful With Comparisons Just because two homes are similar in size doesn’t mean their prices will be similar, too. Variations in age, quality of materials, condition, features, layout, lot size, and other factors can have a significant effect on what a home is worth. The Market Can Change Quickly The market may shift as the number of people selling and buying homes changes. Mortgage rates and local economic conditions also affect home prices. Just because a home sold for a certain amount a little while ago doesn’t mean that home is worth the same today. Motivation Might Matter If you need to move quickly, you may want to factor that into your pricing decision. It’s possible that being more flexible on your price can save you the costs and hassles that come with moving twice or paying two mortgages at once. Allow me to discuss current market data and your real estate goals to help you come up with a winning pricing strategy! Source   It's an incredible time to be alive, especially if you’re into smart home technology. As a real estate professional and tech enthusiast, I’ve seen the rise of smart homes go from an abstract concept to an everyday reality. But as tech evolves, so does the question for homeowners and prospective buyers: When should we upgrade smart home devices? Navigating the tech upgrade labyrinth doesn’t need to be complex or intimidating. It’s about understanding your needs, being aware of tech trends and making informed decisions. When to UpgradeFirst, not every device needs to be upgraded the moment a new model hits the shelves. Devices like smart thermostats, smart lights and even security systems often remain fully functional and useful for years. That said, knowing when to upgrade can ensure you’re not left behind by emerging trends and innovations. It’s also true that sometimes it’s just fun to upgrade. One crucial indicator that it is time to update is when your device no longer supports software updates. Manufacturers often send out software updates and will often warn consumers when a device is no longer supported. When that happens, it is time to consider an upgrade. Without these updates, your device becomes more vulnerable to security risks and may lose compatibility with other devices in your home. Another sign it’s time to trade in for a new model is when the device starts to lose functionality or efficiency. If your smart lock won’t lock from the app on your phone or your security camera’s video quality is degrading, an upgrade can enhance the effectiveness of the device and therefore your overall ecosystem. Performance is also crucial. For example, if your smart speaker takes too long to respond or does not recognize commands, a newer model might offer a significant improvement. What to UpgradeDifferent smart devices have varying life spans and replacement needs. Here are a few key areas to focus on:

Also, remember to recycle or dispose of your old devices properly. Some manufacturers even offer trade-in programs, providing discounts on new models when you return your old device. Staying Ahead of the Tech CurveBeing aware of technology trends can help you make informed decisions about when and what to upgrade. Here are a few tips:

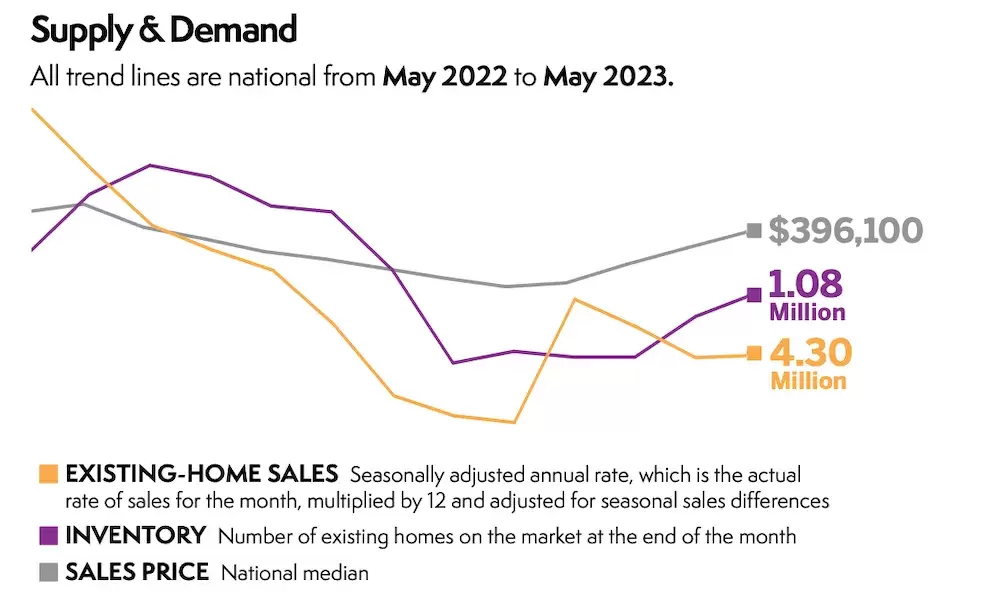

Real estate investors have done well. Rents have risen and home price appreciation has been quite exceptional. In the past three years, the typical rental rate and typical home price have soared by 16.4% and 35.5%, respectively. Over the past five years, those figures are 24.9% and 50.8%. These returns were occurring at a time of low-cost financing. Now it’s time for investors to sell. Home prices have already retreated in some markets—especially in the west, where the median price is 8% lower than a year ago. There are 44 million renter households: Half live in midsized to large apartment buildings, while the other half rent single-family, duplex, triplex or quadplex units. Although apartments are not necessarily as competitive as single-family rental units, a 40-year high in multifamily construction means many units will be hitting the market in the upcoming months and into next year. Rent growth has already turned the corner from acceleration to deceleration, still rising in most markets but at a slower pace. Looking at single-family construction, builders are still underproducing compared to the historical average, but new-home sales are back to pre-COVID levels. Home builders are making profits, stock prices for publicly listed construction companies have risen by around 50% in the past year, and inventory of new homes is plentiful. That’s not the case for existing homes. The latest inventory of 1 million is a historic low, and that’s hindering existing-home sales. Multiple offers are still happening on mid-priced homes. We need 50% growth in listings to reach pre-pandemic 2019 levels. We need 100% growth to reach an adequate supply. This is where investors come in—or rather, come out. The National Association of REALTORS® is calling for a federal incentive to help bring needed inventory to the market: temporary capital gains relief for investors who sell to a first-time buyer or first-generation buyer.   With COVID-19 sweeping across the country, may of us have found ourselves with no job, shortened work hours, or working from home. During this time, many have found themselves needing to cut back on spending and save for the more pressing expenses. Something that has come up is the option for forbearance on your mortgage. The common misunderstanding is that mortgage payments will be waived and disappear into the sunset. THIS CANNOT BE FURTHER FROM THE TRUTH!

Normally, you'll be given two options: (a)temporarily suspend your payments, while still accruing interest at your normal rate, and (b)make payments in smaller amounts Instead, you may have several options to make repayments: 1. Make a lump sum payment at the end of the agreed upon period, with included accrued interest, taxes etc... 2. You can also pay a larger amount each month, to cover the suspended payment amount (this would be ADDED to your normal monthly payment). 3. You can also add the entire amount of suspended payments to your loan balance and extend your loan term. Your options vary by your loan servicer. It is always best to contact them and find out what relief is available to you. All this being said, if you are ABLE to continue making your normal mortgage payments then DO IT. You do not want to fall behind just because you may have the option to. To read more about forbearance, please follow the link below. I can help! TSAHC provides fixed-rate mortgage financing, down payment assistance grants and second liens, as well as mortgage credit certificates for teachers, police officers, corrections officers, fire fighters, EMS personnel, veterans and low and moderate-income households. Their home buyer programs are open to first-time home buyers, as well as repeat home buyers and existing homeowners. Click the logo below to find out if you qualify! Contact me if you have more questions! |

Home is Where Your Investment Is!